Introduction:

Filing income tax returns is a cornerstone of financial responsibility for individuals and businesses alike. It's not just about fulfilling a legal obligation but also about managing finances smartly and ensuring compliance with the tax laws of the land. However, for many, the process can be daunting and confusing. In this guide, we'll break down the essentials of income tax return filing, empowering you to navigate this annual ritual with confidence and ease.

Understanding Income Tax Return: Income tax return (ITR) is a document that taxpayers file with the tax authorities, declaring their income, deductions, and tax liability for a particular financial year. This document provides a comprehensive overview of an individual's or entity's financial activities during the year, serving as a basis for calculating the amount of tax owed or refundable.

Why File Income Tax Return?

Filing income tax returns isn't just about avoiding penalties; it's an opportunity to exercise financial prudence and demonstrate transparency in your financial affairs. Here's why it's essential:

1. Compliance: Filing tax returns ensures compliance with the law, avoiding potential penalties, fines, or legal issues.

2. Record Keeping: It serves as a record of your income, tax payments, and investments, which can be crucial for future financial planning or in case of audits.

3. Claiming Refunds: If you've paid excess taxes or are eligible for tax refunds due to deductions or exemptions, filing a return is necessary to claim them.

4. Financial Discipline: Regularly filing tax returns fosters financial discipline, encouraging individuals to keep track of their income, expenses, and investments throughout the year.

Types of Income Tax Returns:

The type of ITR you need to file depends on various factors such as your sources of income, residential status, and the applicability of special provisions. The Income Tax Department typically releases different forms catering to different categories of taxpayers, ensuring that each entity can accurately report its financial information.

Key Components of Income Tax Return: When filing your income tax return, several crucial components require attention:

1. Personal Information: This includes your name, address, PAN (Permanent Account Number), and contact details.

2. Income Details: Declare all sources of income, including salary, income from house property, capital gains, business or profession, and any other income.

3. Deductions and Exemptions: Claim deductions under various sections of the Income Tax Act, such as Section 80C for investments in provident funds, life insurance premiums, etc., and exemptions like HRA (House Rent Allowance) or LTC (Leave Travel Concession).

4. Tax Payments: Report any taxes already paid, such as TDS (Tax Deducted at Source) or advance tax, and reconcile them with your total tax liability.

5. Verification: Sign and verify the return either electronically or physically, depending on the chosen mode of filing.

Filing Process:

The filing process has become increasingly digitized, offering convenience and efficiency to taxpayers. Here's a general overview of the steps involved:

1. Gather Documents: Collect all relevant documents such as Form 16 (for salaried individuals), bank statements, investment proofs, etc.

2. Choose the Right Form: Select the appropriate ITR form based on your income sources and residential status.

3. Prepare the Return: Fill in the required details accurately, ensuring compliance with the tax laws and regulations.

4. Validate and Submit: Review the filled-in form for errors or omissions, validate the data, and submit the return online through the Income Tax Department's e-filing portal.

5. Verification: After submission, verify the return using any of the available methods, such as Aadhaar OTP, net banking, or sending a signed physical copy to the Centralized Processing Centre (CPC).

Conclusion:

: Income tax return filing is a vital aspect of financial management, reflecting transparency, compliance, and responsible citizenship. By understanding the process, staying updated on tax laws, and leveraging digital platforms, taxpayers can streamline their filing experience and ensure accuracy and efficiency in meeting their tax obligations. So, embrace tax season as an opportunity to take control of your finances and pave the way for a more secure financial future.

Article by Mr.Vishnu M.R

About Digital Signature Certificate (DSC)

The Information Technology Act, 2000 has provisions for use of Digital Signatures on the documents submitted in electronic form in order to ensure the security and authenticity of the documents filed electronically. This is secure and authentic way to submit a document electronically. As such, all filings done by the companies/LLPs under MCA21 e-Governance program are required to be filed using Digital Signatures by the person authorized to sign the documents.

Legal Warning :

You can use only the valid Digital Signatures issued to you. It is illegal to use Digital Signatures of anybody other than the one to whom it is issued.

Classes and types of digital signatures

There are three different classes of digital signature certificates (DSCs) as follows:

Class 1. This type of DSC can't be used for legal business documents, as they're validated based only on an email ID and username. Class 1 signatures provide a basic level of security and are used in environments with a low risk of data compromise.

Class 2. These DSCs are often used for electronic filing (E-Filing) of tax documents, including Income Tax Returns and Goods and Services Tax Returns. Class 2 digital signatures authenticate a signer's identity against a pre-verified database. Class 2 digital signatures are used in environments where the risks and consequences of data compromise are moderate.

Class 3. The highest level of digital signatures, Class 3 signatures require people or organizations to present in front of a CA to prove their identity before signing. Class 3 digital signatures are used for E-Auctions, E-Tendering, E-Ticketing and court filings, as well as in other environments where threats to data or the consequences of a security failure are high.

The Ministry of Corporate Affairs has stipulated a Class-II or above category signing certificate for e-Filings under MCA21. A person who already has the specified DSC for any other application can use the same for filings under MCA21 and is not required to obtain a fresh DSC.

Where can I use Digital Signature Certificates

For signing web forms, e-tendering documents, filing Income tax returns, to access membership-based websites automatically without entering a user name and password etc. Export and Import Organizations (EXIM organizations) can apply for licenses online which means that they can also file accompanying documents electronically on the Directorate General of Foreign Trade (DGFT) website. Since a Digital Signature Certificate ensures authenticity of the document, DGFT has mandated use of

Validity of Digital Signatures:

The DSCs are typically issued with one-year validity and two-year validity. These are renewable on expiry of the period of initial issue.

Costing/ Pricing of Digital Signatures:

It includes the cost of medium (a USB token which is a one-time cost), the cost of issuance of DSC and the renewal cost after the period of validity. The company representatives and professionals required to obtain DSCs are free to procure the same from any one of the approved Certification Agencies as per the MCA portal. The issuance costs in respect of each Agency vary and are market driven.

However, for the guidance of stakeholders, the Ministry has obtained the costs of issuance of DSCs at the consumer end from the Certification Agencies. The costs as intimated by them are as under:

Obtain Digital Signature Certificate

• Digital Signature Certificate (DSC) Applicants can directly approach Certifying Authorities (CAs) with original supporting documents, and self-attested copies will be sufficient in this case.

• DSCs can also be obtained, wherever offered by CA, using Aadhar e-KYC based authentication, and supporting documents are not required in this case.

• A letter/certificate issued by a Bank containing the DSC applicant’s information as retained in the Bank database can be accepted. Such letter/certificate should be certified by the Bank Manager.

What's the difference between a digital signature and an electronic signature?

Though the two terms sound similar, digital signatures are different from electronic signatures. Digital signature is a technical term, defining the result of a cryptographic process or mathematical algorithm that can be used to authenticate a sequence of data. It's a type of electronic signature. The term electronic signature, or e-signature, is a legal term that's defined legislatively.

A digital signature can, on its own, fulfill these requirements to serve as an e-signature:

The public key of the digital signature is linked to the signing entity's electronic identification.

The digital signature can only be affixed by the holder of the public key's associated private key, which implies the entity intends to use it for the signature.

The digital signature only authenticates if the signed data -- for example, a document or representation of a document -- is unchanged. If a document is altered after being signed, the digital signature fails to authenticate.

While authenticated digital signatures provide cryptographic proof a document was signed by the stated entity and that the document hasn't been altered, not all e-signatures provide the same guarantees.

Conclusion

Digital signatures are a powerful tool in the digital world, providing assurance of data integrity, authenticity, and non-repudiation, the digital signature verifies and ensures whether the document is authentic and comes from a verified source and whether the document has not been manipulated since it was digitally signed. Its identity has been verified by a trusted organization (the CA).

Article by Mr.Jishnu M.N

Understanding GST Output Tax and Input Tax

Goods and Services Tax (GST) is a comprehensive, multi-stage, destination-based tax that is levied on every value addition. It is crucial to understand the concepts of output tax and input tax to navigate GST effectively. Here, we break down these two components.

GST Output Tax

Definition:

Output tax is the GST that a registered dealer is required to collect on the taxable supply of goods and services. This tax is collected from the buyer at the time of sale or supply of goods and services.

Calculation:

The output tax is calculated as a percentage of the sale value of the goods or services. The rate of GST varies depending on the type of goods or services, as specified by the government.

Example:

If a business sells goods worth Rs.1,000 and the GST rate applicable is 18%, the output tax will be Rs.180. The total bill amount for the customer would be Rs.1,180.

Payment to Government:

The business collects this tax from the customers and is liable to pay it to the government. This collected tax is known as the output tax liability.

GST Input Tax

Definition:

Input tax is the GST that a registered dealer pays on the purchase of goods or services intended for business use. This tax is paid to the supplier at the time of purchase.

Input Tax Credit (ITC):

Businesses can claim a credit for the input tax they have paid on their purchases. This credit can be used to reduce their output tax liability. Essentially, ITC allows businesses to deduct the tax paid on inputs from the tax collected on outputs.

Example:

If a business buys raw materials worth Rs.500 with an 18% GST rate, the input tax would be Rs.90. When the business sells its finished products, it can use this Rs.90 as a credit against its output tax liability.

Conditions for Claiming ITC:

1. The purchaser must have a tax invoice or debit note from the supplier.

2. The goods and services must be used for business purposes.

3. The supplier must have deposited the GST with the government.

4. The purchaser must have filed GST returns.

Relationship Between Output Tax and Input Tax

The effective GST payable to the government is the difference between the output tax and the input tax. This ensures that GST is effectively paid on the value addition at each stage of the supply chain.

Net GST Payable = Output Tax - Input Tax Credit

Example:

• Output tax on sales: Rs.180

• Input tax on purchases: Rs.90

• Net GST payable: Rs.180 – Rs.90 = Rs.90

Benefits of GST System

1. Elimination of Cascading Effect: GST avoids the tax-on-tax effect prevalent in the previous tax system by allowing input tax credits.

2. Increased Compliance and Revenue: The requirement to match invoices for claiming ITC encourages compliance and helps increase government revenue.

3. Simplified Taxation: GST consolidates various indirect taxes into a single tax, simplifying the tax structure.

Conclusion

Understanding the concepts of output tax and input tax is crucial for businesses to comply with GST regulations and optimize their tax liabilities. Proper management of these taxes ensures businesses can benefit from the input tax credits and avoid penalties due to non-compliance.

Article by Mrs.Saritha Rajesh

Introduction

The Government of India has raised the Tax Collected at Source (TCS) effective July 1, 2023 rate on foreign remittances under the Liberalised Remittance Scheme (LRS) from 5 percent to 20 percent exceeding an amount of Rs. 7,00,000 (Rupees Seven lakhs) in a financial year. The LRS allows resident Indians to transfer funds abroad up to a specified limit. However, recent developments, including the removal of an exemption for international credit card usage and clarifications regarding certain transactions, have brought about significant changes in the landscape of foreign remittances and their taxation. Let's delve deeper into the details and implications of these updates. TCS will be 5% for amounts exceeding Rs.7 lakh for education and medical treatment abroad. A person can claim this deducted amount while filing taxes as an income tax refund or as credit while computing advance taxes.

Types of remittances and Current TCS rates: -

1.Education loan 0.5% in excess of Rs. 7,00,000/-

2.Any amount for education Other than education loan 5% in excess of Rs. 7,00,000/-

3.Remittance for covering Medical Expenses 0.5% in excess of Rs. 7,00,000/-

4.Overseas Tour Package 20% of the amount

5.Remittance in any other 20% of the amount Case

Exemptions

1.Purchasing units of foreign mutual fund schemes or Exchange Traded Funds (ETFs) will not attract TCS because they do not fall under the Liberalised Remittance Scheme’s jurisdiction.

2.While sending money abroad for educational purposes there is an exemption upto Rs. 7,00,000/-

3.Foreign remittance of any amount towards medical expenditure is also exempt upto Rs. 7,00,000/-

Savings on Foreign Remittance Taxes

1.File your Income Tax Return and demand a refund of the TCS amount deducted if you are a person having no taxable income.

2.File your Income Tax Return and adjust your TCS amount deducted against any tax payable on your income.

Conclusion

The increase in tax on foreign remittances in India can indeed be seen as a measure to ensure proper tax payments from individuals who may be evading taxes by not reflecting high-value foreign transactions on their income tax returns (ITRs). By implementing new tax measures, the Indian government aims to address this issue and improve tax compliance.

Foreign remittances are often made by individuals for various purposes, including buying property in foreign countries. If these transactions are not reported in their ITRs, the government may not be able to tax them appropriately, leading to potential tax evasion. To address this gap, the government has taken steps to increase the tax on foreign remittances, thereby encouraging individuals to report these transactions and pay the appropriate taxes.

By imposing higher taxes on foreign remittances, the government aims to create a stronger incentive for individuals to comply with tax regulations. This measure may help discourage individuals from underreporting or avoiding taxes on foreign transactions. It can also serve as a deterrent to those who engage in tax evasion by hiding assets or income abroad.

It is important to note that while these tax measures aim to enhance tax compliance and revenue collection, their effectiveness may depend on various factors, including the willingness of individuals to comply, the efficiency of tax administration, and the enforcement of relevant regulations. The government's efforts to curb tax evasion through foreign remittances should be seen as part of a broader strategy to strengthen tax governance and increase overall tax compliance in the country.

Introduction

The UAE introduced Economic Substance Regulations in 2019 which was amended by Cabinet of Ministers Resolution No 57 of 2020 concerning Economic Substance Regulations in August 2020.

The regulations require companies in the UAE i.e onshore companies, freezone companies and other business forms which carry out certain activities to maintain and demonstrate an adequate economic presence in the UAE relative to the activities they undertake. The purpose of the regulations is to ensure that UAE entities have sufficient economic activity undertaken within the UAE that is commensurate with the actual profits reported in the UAE. ESR applies to legal persons and unincorporated partnerships registered by a competent authority in the UAE, that carry out one or more relevant activities as defined under ESR (referred to as “Relevant Activities”) across the UAE, including Free Zones and Financial Free Zones (such entities are referred to as “Licensees”).

Relevant Activities

All entities that provide the following services shall be subject to ESR:-

1.Banking

2.Insurance

3.Investment fund management

4.Lease – finance

5.Headquarters

6.Shipping

7.Holding Company

8.Intellectual property

9.Distribution and service center

A UAE business that undertakes one or more of the above activities during the relevant Financial Year is referred to as a Licensee. Where a business carries out one or more of the above activities but is exempt from certain requirements under the Economic Substance Regulations, the entity is referred to as an Exempted Licensee.

Economic Substance Report

This purpose of the Economic Substance Report is to provide the National Assessing Authority with information on the Licensee and the income, expenditure, assets, employees and governance related to its Relevant Activities in the UAE.

Each Licensee must file an Economic Substance Report on a stand-alone basis, irrespective of whether the Licensee is part of a consolidated group for financial reporting or VAT purposes.

A UAE corporate entity that operates through one of more branches registered in the UAE must report the Relevant Activities of itself and those of its UAE branches in one composite Economic Substance Report. The Economic Substance Report must be filed with the Regulatory Authority with which the Head Office is registered. A UAE branch of a foreign entity is not required to file an Economic Substance Report if the Relevant Income of the UAE branch is reported and subject to tax in the jurisdiction of the foreign parent / head office. Where a UAE entity carries on a Relevant Activity through a foreign branch or permanent establishment that is subject to tax in the foreign jurisdiction, the UAE entity should not report (i.e. exclude) in its Economic Substance Report the Relevant Income, assets, expenditure and employees of the foreign branch or permanent establishment.

The Economic Substance Report should be filed electronically on the MoF ESR portal within 12 months from the Financial Year end of the entity.

Non-compliance with the obligation to file an Economic Substance Report before the deadline is subject to a penalty of AED 50,000, and can result in the Licensee being deemed to have failed the Economic Substance Test for the relevant Financial Year. Providing incorrect or false information in the report will also attract a penalty of AED 50,000.

Economic Substance Notification

The purpose of the Notification is to provide the Regulatory Authorities with certain initial information in respect of Licensees and their activities in the UAE for the relevant Reportable Period. The information provided as part of the Notification is a prerequisite to filing an Economic Substance Report for the same period.

Both a Licensee and an Exempted Licensee is required to submit a notification.

The Licensee must report all Relevant Activities undertaken during the Financial Year, irrespective of whether the Relevant Activity was conducted throughout the entire Financial Year.

Each Licensee must file a Notification on a stand-alone basis, irrespective of whether the Licensee is part of a consolidated group for accounting or VAT purposes.

The UAE head office / parent company must file a single consolidated Notification that includes details of all its UAE branches that carry out a Relevant Activity, irrespective of whether the head office itself undertakes a Relevant Activity.

The Economic Substance Regulations Notification should be filed electronically on the MoF ESR portal within 6 months from the Financial Year end of the licensee.

Non-compliance with the obligation to file a Notification before the deadline is subject to a penalty of AED 20,000. Providing incorrect or false information I the notification will attract a penalty of AED 50,000.

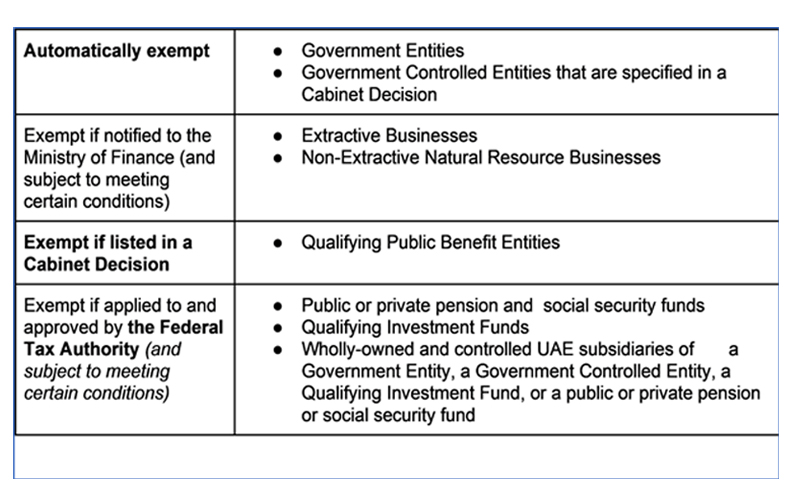

Exempt Licensees

TAXABLE PERSONS

The Corporate Tax Law taxes income on both a residence and source basis. The applicable basis of taxation depends on the classification of the Taxable Person. For instance a Resident Person will be taxed on income derived from both domestic and foreign sources and a Non-Resident Person will be taxed only on income derived from sources within the UAE.

(Person stated above shall be a juridical person incorporated/established/recognised in the state, including a free zone person, or of a foreign jurisdiction that is effectively managed and controlled in the state)

The residential status for Corporate Tax purposes is determined as per specifically mentioned in The Corporate Tax Laws.

EXEMPT PERSON

Certain types of businesses or organizations are exempt from Corporate Tax as mentioned here:-

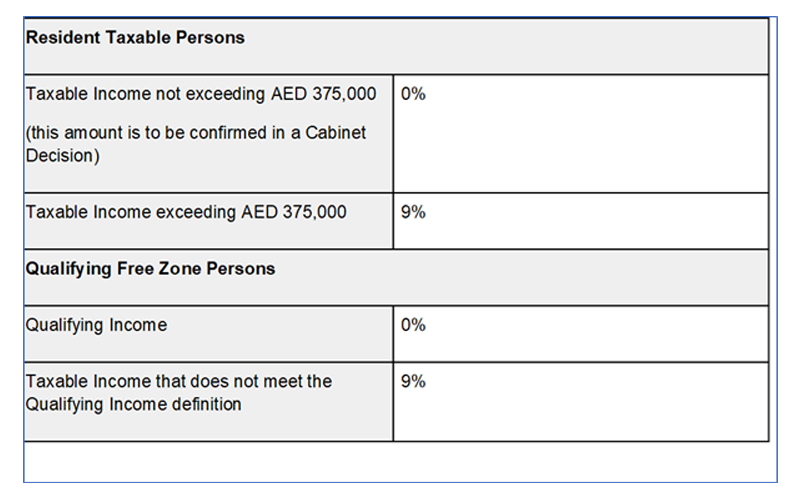

| Effective Date | 1st June, 2023 |

| Scope | All businesses and commercial activities |

| Exemption | Activities involved in extraction of natural resources, Individual's personal income and freezone trading companies |

| Rates | Taxable profits up to AED 375,000 shall be subject to 0% tax rate and taxable profits above AED 375,000 shall be subject to 9% tax rate |

Corporate Tax in UAE

A corporate tax, is a type of direct tax levied on the income of corporations and other similar legal entities. Businesses or companies with taxable income of less than AED 375,000 will have 0% tax rate and for companies exceeding AED 375,000 will have a 9% tax rate.

The taxation will be applied on adjusted profit of a business enterprise.(Adjusted profit = net profit + non cash expenses - non cash gains). This tax is applicable to every establishment irrespective of nationality.

Major Features:

Future for businesses in UAE

Every business and commercial activity will have to adhere to ‘The Corporate Tax Law’ from June 1st, 2023. There is a lot to study and comprehend before the foreign investors feel the pressure. Let's look at the broader picture of this new tax regime to understand its effects.

1.UAE’s corporate tax at 9 % is the world’s third lowest tax rate and one of only three Organization for Economic Co-operation and Development (OECD) member states among the 20 countries with the world’s lowest corporate tax rates. This fulfills its obligation towards OECD, desiring for better investment opportunities and at the same time paves the way for economic development and growth from corporate tax.

2.Corporate tax regime promises long term economic stability and growth, making it more attractive to foreign investors and businessmen.

3.Stable economic environment provides greater confidence for businesses to trust their customers and stakeholders.

4.Corporate tax regime reduces UAE’s dependency on oil reserves and it will help them to diversify their goals to other sectors.

5.Tax collected by the government will reflect in infrastructure, telecommunication, transportation network, water and electricity, research and development etc leading to new demands and opportunities.

6.Increased spending on economic acceleration programs will help small and medium sized enterprises to flourish.

These steps will ultimately fuel the countries’ economic growth and incite businesses to choose the UAE as a base for their operations. The country’s strategic location between the East and West makes it perfect for business and commercial activities to thrive. The country’s move to establish corporate tax is a clear sign of promoting economic growth, trade and investment. Overall, the UAE’s economic prospect looks brighter as a result of this move. Establishment of corporate tax will finally lead to job creation, innovation and economic development.

The CEPA includes a total of 11 service sectors and 100 subsectors. The key sectors are :

| UAE (Trade in Goods) | INDIA | Trade in Services |

|---|---|---|

| Chemicals | Fruits and vegetables | Business services |

| Mineral Fuels | Fish and crustaceans | Construction and engineering |

| Aluminum | Gold and jewelry | Communication |

| Iron and Steel | Cereals | Education |

| Polyethylene | Pharmaceutical products | Environment |

| Copper | Electronics | Finance and Insurance |

| Pharmaceutical products | Healthcare | |

| Plastics | Tourism and travel | |

| Prepared foods | Recreation, Culture and Sports | |

| Glass and glassware | Transport |

1.Market Expansion: CEPA will facilitate increased access to the UAE and Indian markets, creating new opportunities for businesses to expand their customer base and increase sales.

2.Tariff Reduction: The agreement will reduce or eliminate tariffs on a wide range of goods, making imports and exports more affordable for businesses. This can lead to increased competitiveness and profitability.

3.Trade Facilitation: CEPA aims to streamline customs procedures and reduce non-tariff barriers, such as import licensing requirements and technical regulations. This simplification of trade processes will save time and costs for businesses engaged in cross-border trade.

4.Investment Promotion: CEPA provides favorable conditions for investment by offering protections and guarantees to investors. This can attract foreign direct investment (FDI) and promote business development in sectors such as infrastructure, manufacturing, tourism, and technology.

5.Services Sector Growth: The agreement includes provisions to liberalize trade in services, facilitating the entry and operation of businesses in sectors such as banking, insurance, telecommunications, healthcare, and education. This can lead to the development of new service offerings and market expansion for service providers.

6.Intellectual Property Protection: CEPA strengthens intellectual property rights (IPR) protection, ensuring that businesses' innovations, patents, trademarks, and copyrights are safeguarded. This encourages research, development, and innovation, fostering business growth and competitiveness.

7.Collaboration and Knowledge Transfer: CEPA encourages collaboration and cooperation between businesses in both countries. This can lead to partnerships, joint ventures, and knowledge sharing, promoting innovation, technology transfer, and overall business development.

The impact of CEPA on business development is expected to be positive, creating a conducive environment for trade, investment, and collaboration between the UAE and India. It offers opportunities for market expansion, cost savings, increased competitiveness, and access to new sectors, stimulating business growth and economic development.

India’s trade relationship with UAE dates back to about 5000 years. The very strategic location of UAE has brought India closer with respect to trade and commerce. Indian merchants from the Indus Valley brought timber, spices and grain, while merchants in modern-day Sharjah and Ras Al Khaimah in the UAE traded copper, pottery and beadwork. It's no wonder that these two countries reflect each other's food, fabric, architecture and culture over the course of thousands of years.

Even though these two countries are independent now, they do share a deep connection. The highest number of foreign expats in the UAE are Indian migrants. Over 38 % of UAE population include Indians. The colorful relationship between India and UAE can be explained with respect to the kind of trade and commerce these countries are involved in. UAE is India’s third largest trading partner with bilateral trade worth US$ 59 billion for the year 2019-20. UAE is also India’s second largest export destination with export value of US$ 29 billion for the year 2019-20. Not only this, UAE has made an investment of US$ 18 billion in India and India has invested about US$5 billion IN UAE.

A Comprehensive Economic Partnership Agreement (CEPA) was signed on 18th February,2022 to strengthen and make the best of the relationship between India and UAE.

So what is CEPA?

Benefits of CEPA between India and UAE.

| 1 | Economic Partnership | Specialized economic zones in logistics and services, pharmaceuticals, medical devices, agriculture, agri-tech, steel, and aluminum |

| 1 | Cultural Cooperation | India-UAE Cultural Council to promote cultural co-operation between the two countries |

| 3 | Energy Partnership | Working together to achieve a just and equitable transition to a low-carbon future |

| 4 | Climate Action and Renewables | Joint Hydrogen Task Force to assist in the scaling up of technologies. |

| 5 | Emerging Technologies | Fintech, edutech, health care, logistics and supply chain, agritech, chip design, and green energy are some of the areas |

| 6 | Food Security | Promote and strengthen infrastructure and dedicated logistics services that connect farms to ports and then to final destinations in the UAE |

| 7 | Skill Cooperation | Create a set of professional standards and skills framework that they both agree on. |

| 8 | Education Cooperation | Establish an Indian Institute of Technology in the United Arab Emirates |

| 9 | Defense and Security | Boost bilateral cooperation in the fight against terrorism, terrorist financing, and extremism. |

| 10 | Cooperation in International Arena | Strengthen bilateral cooperation in multilateral areas to promote economic and infrastructure cooperation. |

India and the UAE have signed a historic trade and economic agreement that will propel the two friendly nations towards a glorious, shared future. CEPA between India and the UAE is a historic deal that will transform the lives of millions of people in the two countries. This ground-breaking agreement will facilitate the free flow of goods, services, capital, technology, and people, as well as mutually beneficial collaboration. CEPA has the capacity to change the destiny of these two countries.

We are a team of experienced professionals providing services such as Financial Consulting, Management Consulting, Tax Advisory, Investment Advisory, Risk Advisory, Audits, Incorporation Services, Accounting and Book Keeping Services etc.

© 2022 Vinstreak Consulting Pvt.Ltd. - All Rights Reserved | Powered by Qunexa Infosolutions Pvt.Ltd.